Global X ETFs China Update

In the first half of 2023, our investment team had six analysts make 25 trips to mainland China to meet with management teams, visit production centers, and interact with local policy makers. Overall, feedback centered on fits and starts across China’s broad economy, with specific opportunities in long-term secular trends such as energy transformation, manufacturing upgrades and automation, and enhancing self-reliance. The combination of a high savings rate, pent-up demand, and a loosening of regulatory measures has improved sentiment across most management teams we spoke with. From a demand perspective, it seems the market’s expectations for a post-reopening rebound were too lofty in the first half of the year. Forecasts have come down, but our on-the-ground research suggests that the reopening remains steady, and any signs of deeper fiscal or monetary stimulus could drive an unexpected re-rating. In this article, we examine the first half of 2023 and look at what the second half of the year may hold for various sectors in the large and diverse Chinese economy.

Key Takeaways

- Although China’s recovery in the first half of 2023 undershot lofty expectations, our on-the-ground research suggests that the reopening is steady.

- We remain optimistic about the long-term attractiveness of China’s shift toward higher quality, consumption-driven growth.

- Any signs of deeper fiscal or monetary stimulus could drive an unexpected re-rating of Chinese equities.

Near-Term Outlook

China’s policy pendulum historically swings from tightening to loosening over a shorter time horizon versus typical U.S./European cycles. This reflects the Chinese Communist Party’s (CCP) desire to control the economic backdrop and deliver consistent economic growth. Given its far-reaching powers, the Chinese government has multiple levers beyond traditional monetary and fiscal policies, which means the market should not underestimate the CCP and its potential impact on China’s equity market.

China’s post-reopening recovery has been slower and bumpier than expected, but ongoing recovery will probably remain underway for the balance of 2023. Within consumption, the service sector has experienced the most significant recovery since reopening, as consumers flocked back to dining and tourism activities. Elevated activity levels are expected to flow into earnings over the next few quarters.

Though the weak job market data amongst younger age demographics have taken headlines, the overall unemployment rate has actually fallen since reopening, showing improvements are underway.1 As job creation continues to increase across the country, we could see more broad-based improvements in consumer confidence and consumption.

However, for consumer and business confidence to meaningfully rebound, the onus appears to be on policymakers to re-establish confidence by implementing measures such as incentives for investment or introducing stimulus initiatives. While lower borrowing rates and the recent tax exemption for electric vehicle purchases beyond 2023 are positive steps, other potential measures include relaxing home purchase restrictions, increasing infrastructure support, or offering targeted consumer incentives. Due to the growth slowdown in 2Q23 and concerns surrounding local government debt, we expect policymakers to maintain an accommodative stance in the upcoming quarters to reduce the negative output gap, with more significant moves potentially coming soon.

Parts of China’s economy may need a few more years to fully digest the excesses and rapid growth of the past decade. Still, we remain optimistic about the long-term attractiveness of China’s shift toward higher quality, consumption-driven growth. China’s household saving rate peaked in 2010 and has generally declined since then.2 Similarly, private consumption expenditure as a percentage of GDP bottomed in 2010 and has since gradually increased.3 While the pandemic temporarily disrupted this trend in recent years, the structural trend has not changed. As reopening continues, we expect to see private consumption driving economic growth again this year.

Big Picture: Evolving GDP Growth Drivers

GDP = Private Consumption + Government Spending + Private Investment + Net Exports

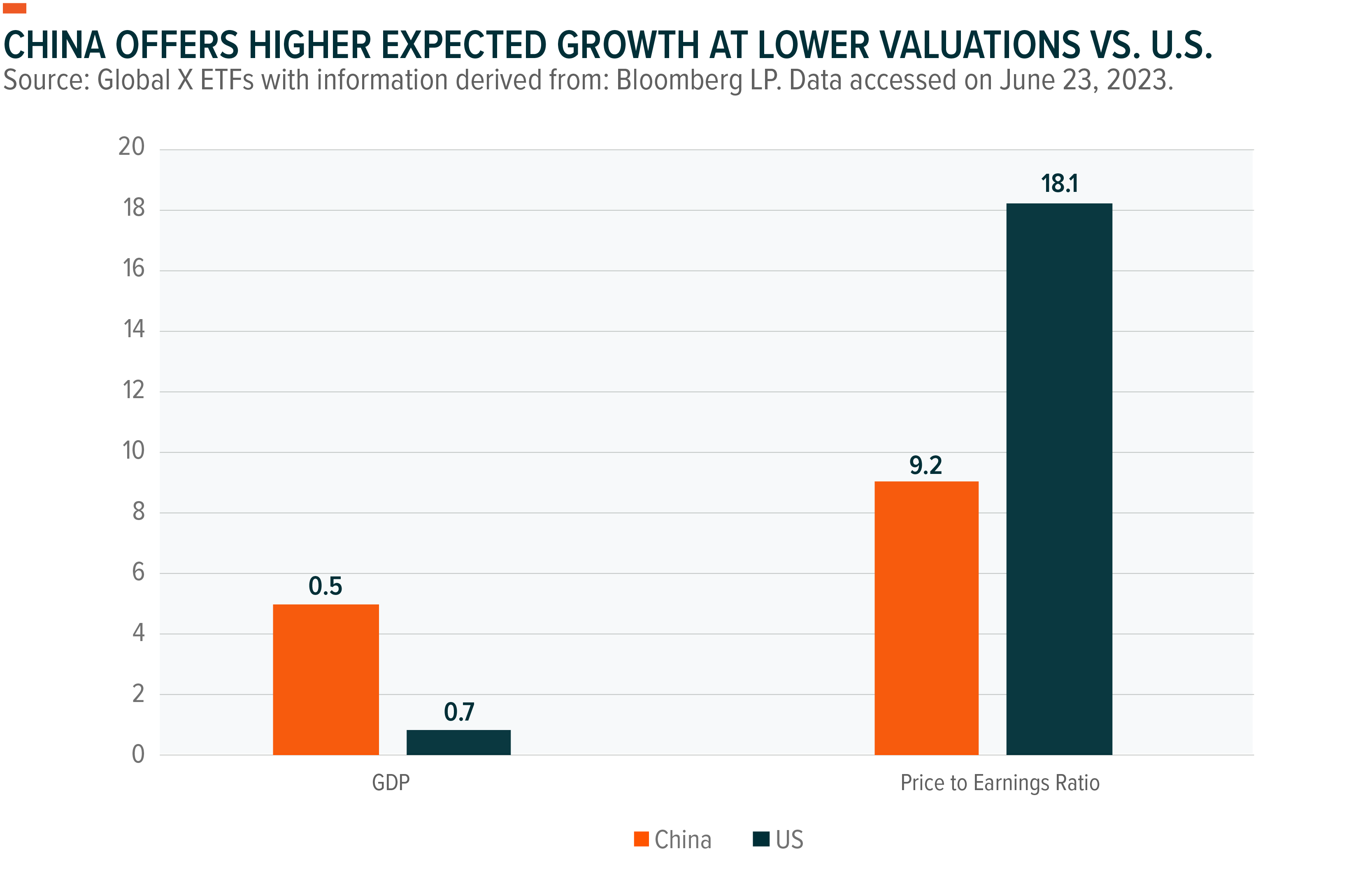

Government spending cannot last forever; exports (as a % of GDP) should diminish, as countries do not want to rely on outside forces; and private investment is dependent on business cycles. That leaves private consumption as the primary piece emerging market (EM) governments have left to control in order to drive GDP expansion. With roughly 68% of GDP growth coming from private consumption, the U.S. has set a model for a sustainable economy.4 China (where private consumption accounts for roughly 38% of GDP) has watched, learned, and begun to emulate this model.5

China’s common prosperity initiative (“Common Prosperity”) provides a clear example of this shift to private consumption as the key driver of sustainable growth. China has experienced tremendous economic growth, but it has come with a rise in social inequality and economic disparity. Common Prosperity is a development plan aimed at promoting domestic-oriented long-term growth.

The Chinese government understands that it must move its economy up the value chain, create higher-paying jobs, grow its middle class, and improve growth through consumption. This starts with moving capital allocations away from construction and low-level manufacturing to higher value-add production.

Virtuous Growth Cycle Could Be Emerging

With old economy sectors providing less forward-looking ammunition to drive GDP growth, China’s government has shifted its focus to technology and sustainability. Investments in these areas ought to help drive growth on their own, but they could also drive higher wages, leading to increased domestic consumption, which could create a virtuous cycle. This cycle would likely make up for the slowdown in exports, real estate investment, government spending, and low-end manufacturing. With falling birth rates, China sees fewer annual new workers enter the labor force. The government understands that a sustainable future requires a shift from quantity to quality. That means increasing value and productivity similar to what other countries did through the 20th century. Over the next five years, 50 million graduates are set to enter the workforce in China, more than the U.S., Germany, Japan, Korea, and Southeast Asian countries combined.6 The playbook is there, and China’s increasingly educated workforce appears well prepared for this transition.

That said, for the second half of this year, various sectors also have their own idiosyncratic drivers, which we discuss below.

Consumer Discretionary

- China’s consumer discretionary sector (as measured by the MSCI China A Consumer Discretionary Index) has recovered from 2020’s trough but remains well below peak levels reached in early 2021.7 For some verticals, such as travel, apparel, and cosmetics, revenue has already recovered sharply, mainly driven by traffic rather than spending per customer.8 As this implies, consumer confidence is still somewhat soft, but we see room for further improvement.9

- According to the National Bureau of Statistics, growth in retail sales in May slowed to 12.7% year over year from 18.4% in April.10,11 The market will closely watch for potential stimulus policies to boost the economy, since June-September will see a high base.

- Following the People’s Bank of China’s open market operations (OMO) and medium-term lending facility (MLF) interest rate cuts, Premier Li Qiang hinted that a basket of growth-promoting measures could be announced soon.12 China’s National Development and Reform Commission (NDRC) is also said to be contemplating measures to boost consumption.13

Consumer Staples

- Overall, consumer confidence remains subdued with room for improvement.14 As a result, high household savings have not translated into consumption yet.

- We see opportunities for continued growth in consumer staples, led by a rebound in services and strong demand for food & beverages, as China continues to reopen.15

- Government rhetoric around boosting GDP growth has generally centered around domestic consumption. Incremental fiscal and monetary expansion could bode well for the sector.

Energy

- We expect to see some broader support for energy prices as we start the second half of 2023, based on both supply and demand.

- From the demand side, although we envision developed market GDP slowing down, it appears that the U.S. Federal Reserve could be close to the peak of its rate hiking cycle, which could offer a boost to the U.S. economy. China’s reopening may also revive demand not present in 2022.

- From the supply side, major oil companies have significantly cut down capital expenditures over the past few years and continue to do so.16 Alternative energy production has not yet reached the point where it can fully make up for the shortfall. This, combined with OPEC+ production management and continued war in Ukraine, could lend support to energy prices.

Financials

- We anticipate a gradual recovery in retail credit growth, driven by consumption, and expect steady mortgage growth in the second half of the year, after signs of improving infrastructure and industrial credit growth in the first half.17

- We expect more policy stimulus to come in the back half of 2023. However, whether it could be in structural sectors (such as electric vehicles, tech hardware, etc.) or more of a shift towards property will be important to watch.

Information Technology

- Demand for consumer electronics has been gradually improving, and sales growth has turned positive in 2023.18 Meanwhile, the sector has also been destocking since 2H22 and inventory levels have fallen, which could signal a bottoming out of the downcycle.19

- We feel that resilient capex guidance from U.S. cloud service providers, along with investments in artificial intelligence (AI), could bode well for the AI computing power supply chain. This could offset weakness in the general-purpose server market.20

- Semiconductor equipment may remain in a sweet spot, as it could continue to benefit from localization opportunities.

Healthcare

- After a weak 2022, healthcare service companies are seeing a visible demand recovery.21 We see potential long-term growth opportunities for leading private healthcare service providers against a backdrop of low penetration, rising medical demand, and hospital capacity expansions.

- We expect the traditional Chinese medicine (TCM) industry to experience high-quality growth over the next few years, potentially benefitting from supportive policies. The new 2022 National Reimbursement Drug List (NDRL) took effect on March 1, 2023 and included 2,967 drugs: 1,586 western drugs and 1,381 finished TCMs.22 However, we believe it’s important to monitor possible intervention in areas not aligned with government views on Common Prosperity.

Industrials

- China continues to prioritize advanced manufacturing and automation development. As such, the industrial sector should enjoy strong policy tailwinds to support research & development and adoption.23

- We see a strong appetite for local enterprises to adopt Chinese equipment and digital solutions to tackle heightened geopolitical tensions, most notably with the U.S. Moreover, China will likely restructure its science and technology ministry to channel more resources to achieving important breakthroughs, with the goal of moving faster towards self-reliance.24 Thus, we expect to see Chinese industrial players’ market share grow further.

- The country’s foreign infrastructure development effort, known as the Belt and Road Initiative, is likely to stand out as one of the major themes for the second half of 2023.

Materials

- Lower-than-expected industrial production activity and ongoing property sector weakness have weighed on demand for construction materials such as steel.25 However, for metals like aluminum, prices have been more resilient since March, as limited supply in China and Europe has cushioned prices from correction.

- We expect margins on glass to stay elevated, as the government’s efforts to boost housing completion remain in place. Meanwhile, demand and supply recalibration could support prices for solar glass.

- Electric vehicle production momentum is picking up, and our research suggests that downstream cathode customer inventory levels still appear low.26 As a result, we see potential opportunities for lithium names in the China materials sector.

Real Estate

- In our view, weak demographics, a lack of speculative demand, and limited confidence on job security/income expectations are likely the main reasons for the underwhelming property sales recovery. Unless we see a pick-up in stimulus, we envision flattish property sales in 2023.

- In our view, a key risk for the sector is that short-term government support could remain limited.

Utilities

- Renewable energy capacity is being installed quickly, and solar installations have accelerated, due to the recent drop in polysilicon costs.27 Wind installations have accelerated, aided by declining turbine costs.28

- Falling coal prices have driven a rebound in profitability and prices of independent power producers, especially those that are heavily reliant on coal.29 A rebound in energy prices could hurt projections, however.

- A weakening long-term outlook for gas demand is possible, as China appears to be putting less emphasis on switching energy use into natural gas for energy-security reasons.

Communication Services

- Developments in generative artificial intelligence could not only reduce costs, but also improve content.

- The gaming and entertainment sector has seen license approval normalizing, with 80-100 video games approved every month.30 For 2H23, we expect new game releases to drive industry revenue growth.

Conclusion

Expectations for China’s post-COVID-19 reopening did not live up to investors’ lofty expectations in the first half of 2023. However, we have seen pockets of strength and believe that the myriad structural growth drivers we see in the country remain in place. The nation’s recovery following strict COVID-19-related lockdowns is unlikely to proceed in a linear fashion, but our time on the ground suggests that the reopening is ongoing, presenting potential opportunities for investors.