Japan’s Robot Dominance

PreviewListen

Beginning in the 1960’s, the rise of manufacturing for the automotive industry and the concomitant rise of industrial robots played an indispensable role in powering Japan’s economic miracle. By the 1980’s, the momentum accelerated to the point where commentators began referring to 1980 as “year one” for Japanese robotics. These forces culminated in Japan being dominant in the field of robotics today.

In this piece, we dive into the world of Japanese robotics, including answering several key questions:

- How did this industry take shape?

- Which segments of the robotics theme does Japan have an advantage in today?

- How can robotics help Japan grapple with several current and future challenges, including population decline, economic doldrums, and COVID-19?

Industrial robots powered Japan’s economic miracle

Early signs of brilliance emerged after the 1964 Olympics

Rapid economic growth was the zeitgeist of Japan in the 1960’s. Prime Minister Ikeda Hayato boldly pushed the income doubling plan, the expansion of domestic manufacturing was in full swing, and the 1964 Tokyo Olympics became a symbol of national revitalization. This was the backdrop against which Japan’s robot industry took its first steps.

In America, the company Unimation partnered with General Motors to deploy the first industrial robot, the Unimate, in 1961. Unimation’s decision to form a partnership with Kawasaki Heavy Industries in 1968 proved to be a fateful moment for industrial robotics in Japan, and only a year later the Kawasaki-Unimate made history as Japan’s first domestically produced industrial robot.1 In this nascent phase, Japanese companies largely relied on research and designs supplied by American partners.

Fanuc, a future giant in industrial robots, was mostly focused on numerical controls (NCs) throughout the 1960s and did not begin robots until the 1970s.2 Among other future Japanese leaders in robotics, Daifuku derived most of its growth in the 1960s from overhead Webb Conveyor systems, while Mitsubishi Electric was already a Fortune 100 global company that manufactured a wide range of electrical products.3,4

In the 1960’s, rising incomes and purchasing power translated into rising demand for personal automobiles. At the same time, Japan faced a labor shortage despite rapid urbanization that brought young workers from the countryside to the city. The shortage meant that it was difficult to find workers, but it was even more difficult to find skilled workers able and willing to perform “3D” jobs (dirty, dangerous, degrading) in auto plants, like welding and painting. Furthermore, the norm of lifelong employment and strong job security at Japanese companies meant that workers felt less threatened by the introduction of robots and automation.5 All of these factors incentivized automation in car factories.

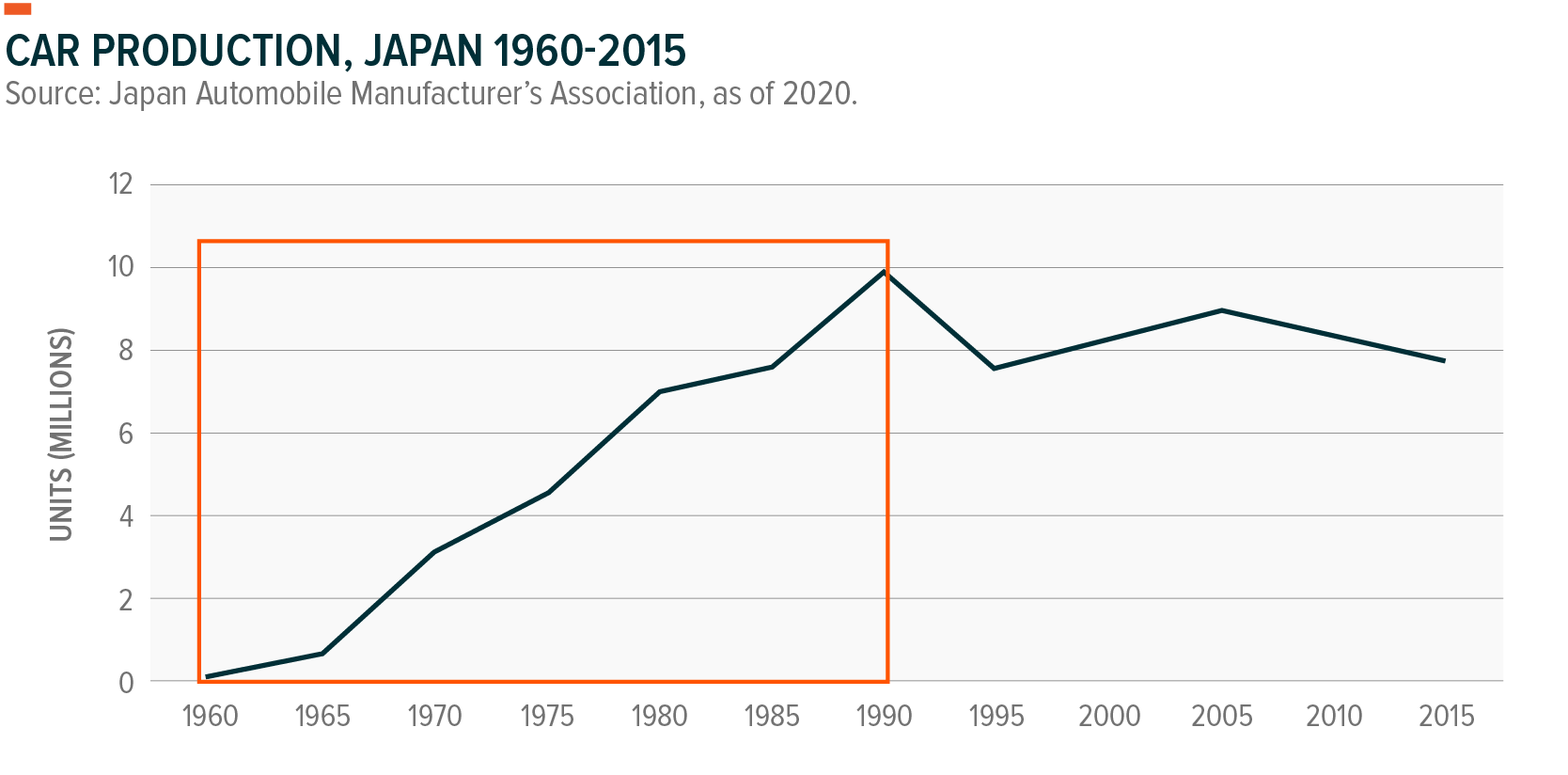

Japan’s auto industry experienced rapid growth in the post-war era up until the collapse of the Japan bubble. Industrial robots became very useful for arc- and spot-welding as well as application of paint on car assembly lines.

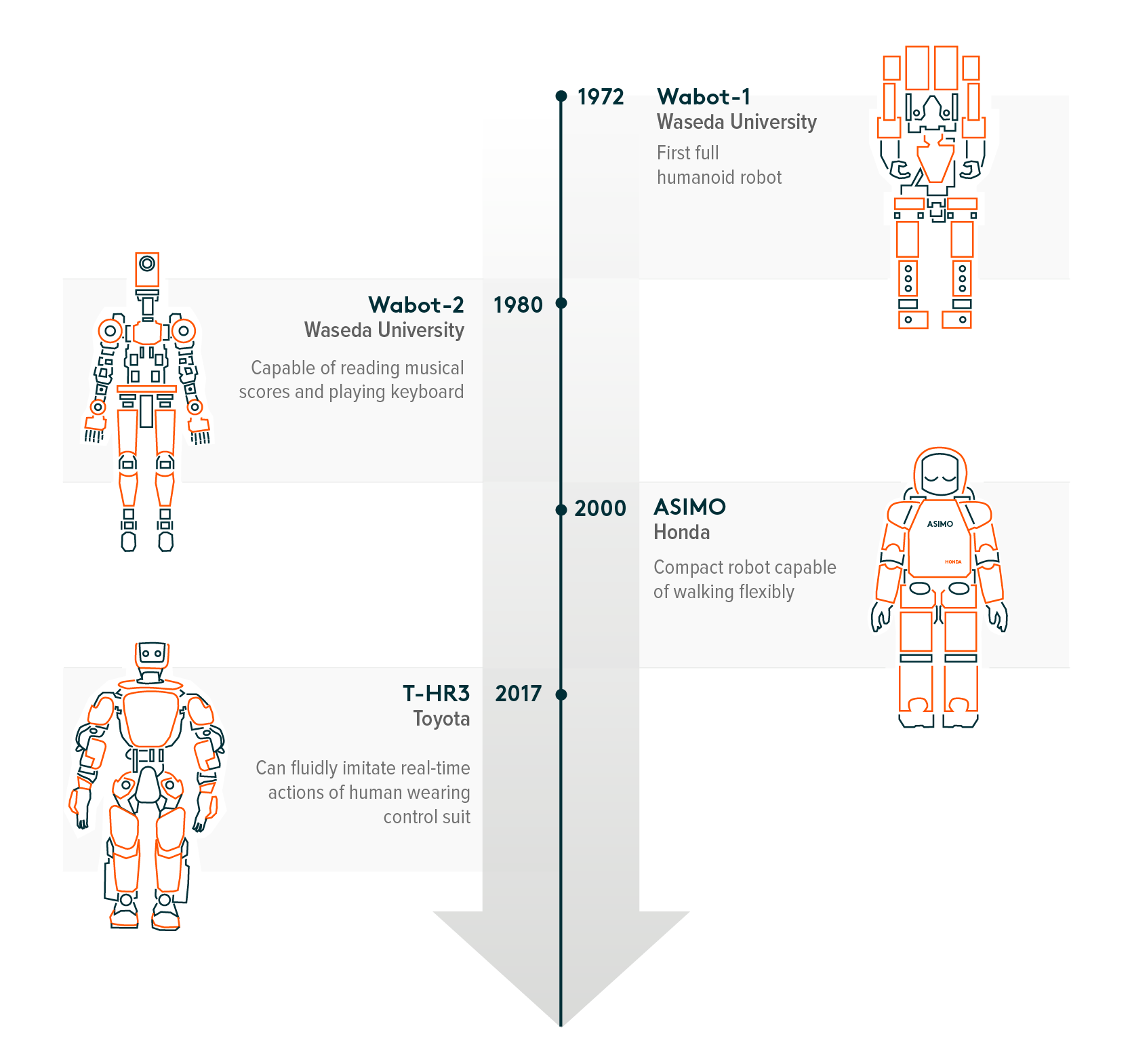

While the robot arms of Kawasaki toiled away at automotive assembly lines, Waseda University became a pioneer in the field of humanoid service robots. Waseda researchers experimented with walking leg prototypes throughout the 1960’s and created the first full humanoid robot, the Wabot-1, in 1972.

From Waseda University’s Wabot-1 to Toyota’s T-HR3, Japan’s humanoid robots have come a long way.

1980 became “year one” for Japanese industrial robots

By the 1980’s, Japan’s competitive power and innovative potential was abundantly clear. This was certainly the case for Japan’s robotics industry as well. Japan’s economic growth moderated after the impact of two oil shocks and trade tensions with the US shifted the calculus of business leaders, but it was nonetheless an era of opportunity for Japanese robot makers as they became more independent technologically and more international in their reach.

The rapid expansion of robotics during this era is why Japanese commentators today often refer to 1980 as “year one” for robotics.

One of the contributing factors to this expansion was the switch from hydraulic robots to electric robots. The transition from DC servo motors to AC servo motors and advances in microprocessors made a higher degree of precision possible.6 Professor Hiroshi Makino’s invention of SCARA (Selective Compliance Articulated Robot Arm) robots was a testament to Japan’s innovative capacity. Increasing technological prowess helped Japanese robot makers expand their reach in the 1980’s. While Fanuc relocated to its now somewhat-famous headquarters at the base of Mount Fuji and established a remunerative partnership with General Motors, Daifuku expanded into automation for semiconductor fabs and built out a presence in Canada, Singapore, and the UK.7,8

Robotics stayed strong amid economic malaise of post-bubble Japan

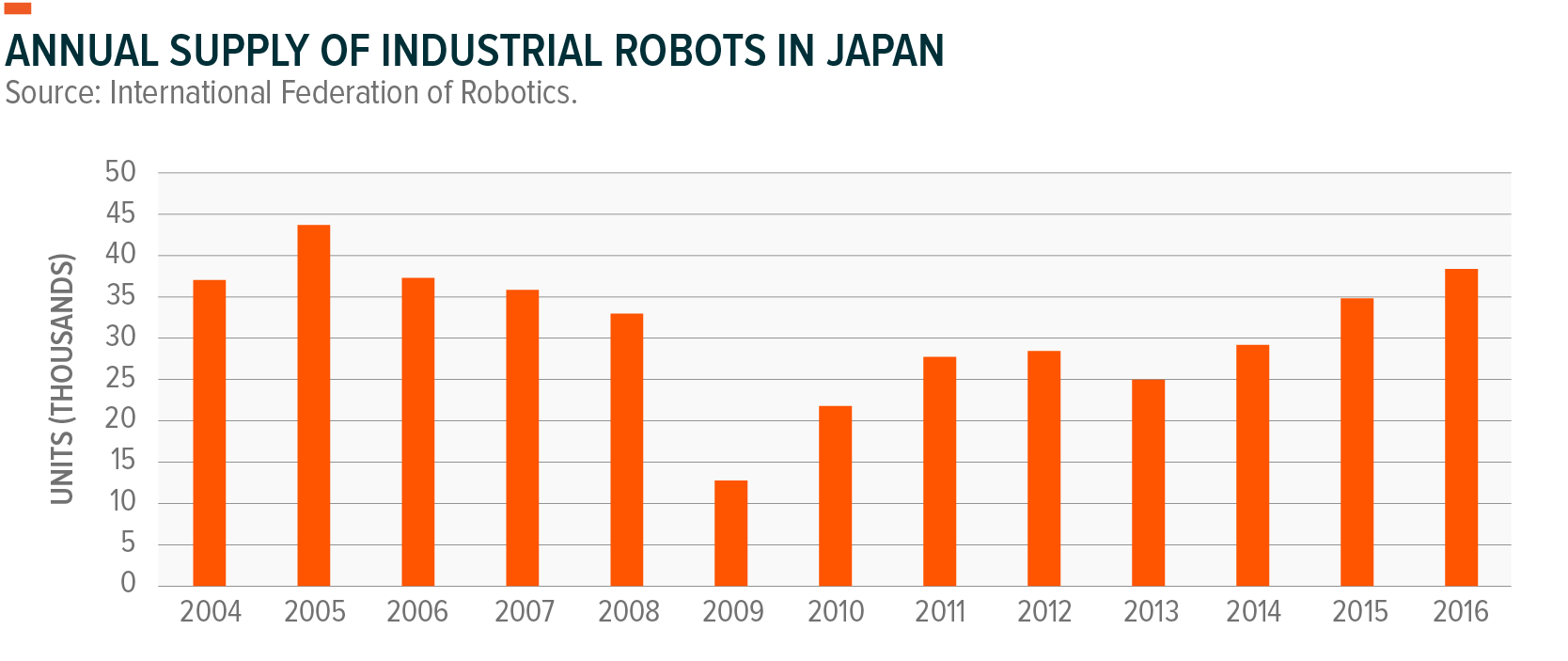

Japan’s economic miracle lost steam after the collapse of its housing bubble in 1991, which kicked off what has come to be known as the lost two decades for Japan’s economy. Data on yearly global supply of robots reveals that robot makers were not unscathed: a sudden drop in 1992 was followed by two years of stagnation.9 While Japanese firms tried to recoup lost opportunities, the sudden rise of personal computers and the internet drove up demand for semiconductors, which created new opportunities for robot makers, and sales remained strong until the global financial crisis.

The supply of industrial robots in Japan took a hit during the “double punch” of the 2008 Great Financial Crisis and 2011 Tohoku Earthquake.

Despite challenges from the collapse of Japan’s bubble, the country’s manufacturers boasted 90% of global robot sales in the 1990s.10 Japan’s domestic semiconductor industry began its relative decline around this period, but growth in the global semiconductor industry was a boon for Japanese robotics. It became increasingly difficult for humans to work with wafers, or slices of silicon used to manufacture miniature semiconductors, and semiconductor factories needed immaculate dust-free cleanrooms.

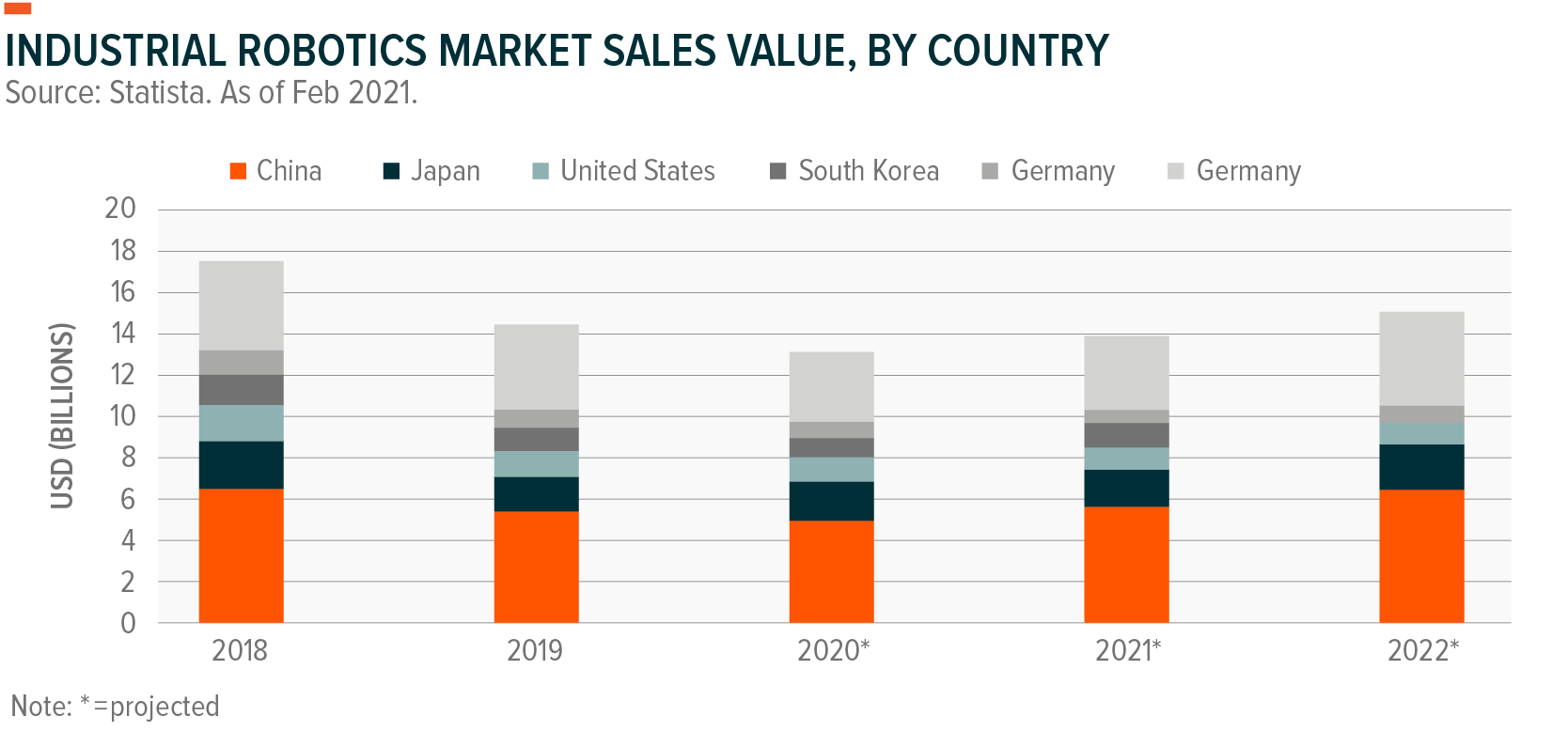

When it comes to demand for industrial robots, the center of gravity rapidly shifted towards China in the early 2000’s as it experienced its own economic miracle. Most demand for industrial robots today comes from China and Japanese robot makers have adjusted their strategies accordingly.

China is now a major source of demand for industrial robots and revenue for Japanese robot makers.

Japan maintains dominant position in current robotics landscape

Today, Japan is a veritable superpower in the field of robotics, with 47% of global robot manufacturing as of 2020.11 The image of Japan as a high-tech country is inseparable from its success in robotics.

Which companies lead in industrial robotics?

Fanuc, Yaskawa, Kawasaki, Daifuku and SMC are just a few of Japan’s leaders in industrial robotics. As of the end of 2020, these five companies had a combined market capitalization of roughly $120bn. Fanuc and Yaskawa alone have a market share of 29.5% in the global industrial robot market, as of 2019.12

- Fanuc’s iconic yellow robot arms can be found in factories around the world. The number of Fanuc robots made is indicative of its strength; the company set an industry milestone in Jul 2021 by manufacturing its 750,000th industrial robot.13 Fanuc’s founder, Dr. Seiuemon Inaba, was a pioneer in numerical control (NC), and computerized numerical control (CNC) continues to be a key component of Fanuc’s business portfolio to this day, with the company holding 50% of the global CNC market as of 2020.14

- Yaskawa started out in 1915 as a manufacturer of electric motors and that legacy remains part of its business portfolio in 2021. What truly differentiates Yaskawa is its strong position in the servo motor market, in which it is a global leader. Servo motors allow machines to rotate and move with a high degree of precision, which makes it a key component for many robots. Yaskawa is also a competitive manufacturer of robotic arms. Recently the company is pursuing a digitalization strategy called YDX (Yaskawa Digital Transformation).15

- Kawasaki’s fateful partnership with Unimation gave it a first-mover advantage in Japan’s industrial robot market. Kawasaki remains a leader in robotics to this day, but it is not a pure-play robotics company. Its vast portfolio covers aerospace systems, motorcycles, and precision machinery among other segments.16 Only 13.2% of its revenue came from precision machinery and robotics in FY2020.17 Likewise, Mitsubishi Electric is a major player in robotics, but draws in much of its sales from other segments.

- Daifuku is a leader in the field of factory automation (FA), particularly intra-factory logistics. Most of Daifuku’s sales are derived from storage and transportation systems for factories, production lines for cleanrooms and automobile plants, and automated systems for airports.

Automakers are also a competitive force in robotics

Given the close ties between robotics and the auto industry, it is only natural for some carmakers to have a foothold in robotics. Contrary to what one might expect, these automakers do not singularly focus on robots for automobile plants.

Honda’s groundbreaking progress in humanoid robots is a good example. Honda’s experiments in self-regulating bipedal robots throughout the late 80’s and 90’s culminated in the unveiling of ASIMO in 2000. Videos of ASIMO climbing stairs, performing dance moves and acting as a waiter captivated the public’s attention.

Meanwhile, the Toyota Research Institute (TRI) powers much of Toyota’s strides in robotics. Much of the TRI’s work focuses on collaborative robots that can “augment human abilities” by working alongside them.18 Some of TRI’s recent work includes a household robot that hangs from the ceiling, and the T-HR3 humanoid robot that can gracefully mimic actions of a user wearing a control suit.

Japanese companies boast a global footprint

Factories around the world rely on Japanese robots to automate certain processes or even entire production lines. As Japanese robot makers became more technologically independent in the 80’s, the appreciation of the Japanese yen following the Plaza Accord in 1985 gave them even more of an incentive to move production abroad.

Fanuc, Daifuku and the robotics division of Kawasaki all have their US headquarters in Michigan. This is no coincidence; Detroit, Michigan was once the heart of automobile production in America.

Revenue breakdown by geography (as of Oct 8, 2021)

- Fanuc: Japan 15.0%, China 33.1%, United States 18.8%, Europe 15.5%

- Daifuku: Japan 34.6%, China 12.6%, Americas 28.6%, South Korea 9.2%

- Kawasaki: Japan 47.3%, Asia 18.6%, United States 21.1%, Europe 9.6%

- Yaskawa: Japan 34.9%, China 25.1%, Americas 15.1%, Europe/Middle East/Africa 14.1%19

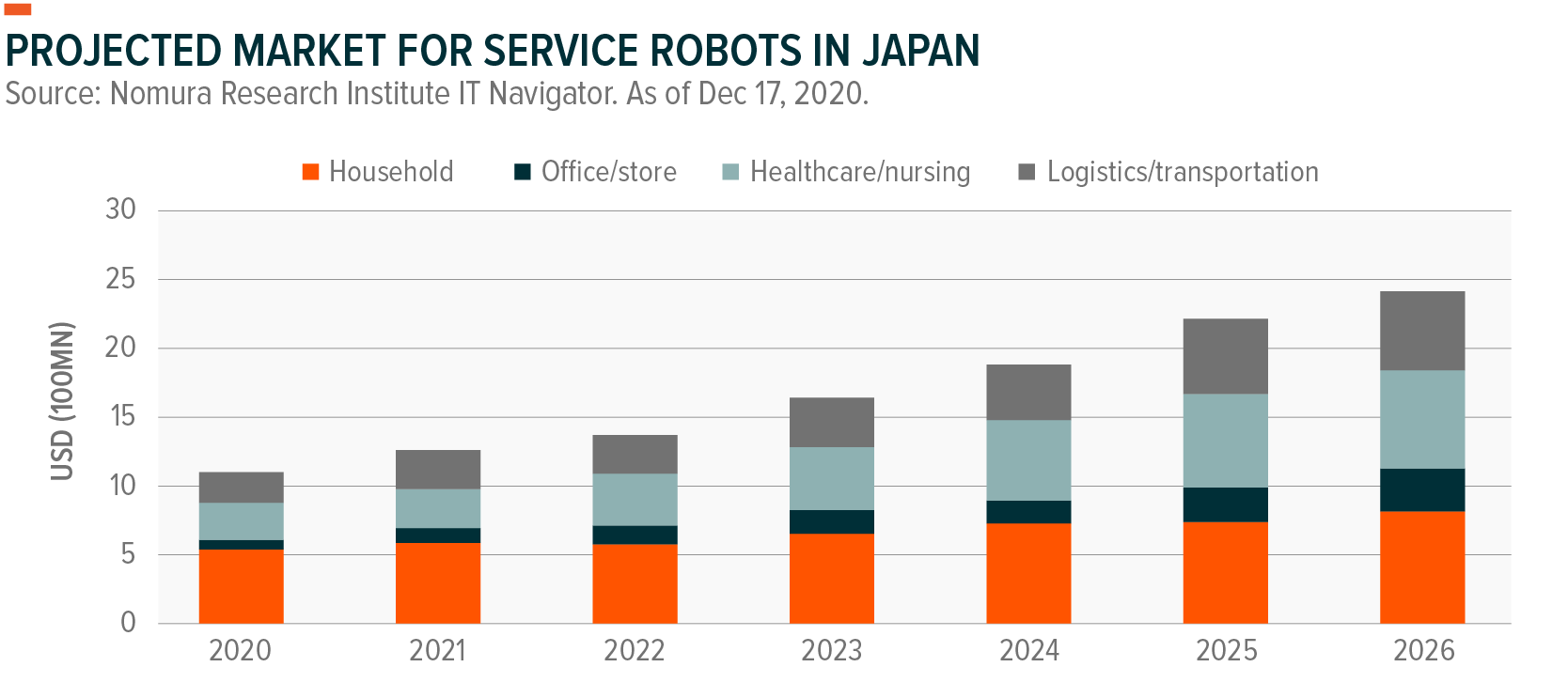

Will 2021 be “year one” for Japanese service robots?

Industrial robots propelled Japan’s economic miracle and should continue to be paramount towards reviving Japan’s economy. However, the landscape is beginning to shift as unique social and economic needs drive rapid growth in a new category: service robots. Just as 1980 became year one for industrial robots, 2021 may very well become year one for service robots in Japan, as they make inroads into areas like healthcare, hospitality, transportation, and domestic tasks.

2020 Olympics intended to be opening of a new era

As early as 2014, Japanese policymakers were already concocting plans to make 2020 the year to showcase the future of Japanese robots. Then-Prime Minister Abe even publicly suggested hosting a Robot Olympics alongside the 2020 Olympics. In some respects, it was supposed to herald the start of a new era.

The Ministry of Economy, Trade and Industry’s (METI) New Robot Strategy, approved in 2015, explicitly laid out plans to prepare the robotics industry for that moment. Among other things, METI’s strategy emphasized the importance of leading the world in the application of robots and integrating robots with the Internet of Things, while also proposing the idea of a “robot barrier-free society.” In essence, a “robot barrier-free society” would mean a dramatic rise in service robots, like care robots in nursing homes, greeter robots in stores and even wearable robots to assist with tasks like lifting heavy items.

The unexpected shock of the COVID-19 pandemic derailed the original plans for the Olympics, but even under adverse conditions, the world still had a small glimpse of what such a society may look like. Toyota developed robot versions of the Olympics mascots, Miraitowa and Someity, that were supposed to shake hands with and dance in front of spectators. Meanwhile, Panasonic prepared a wearable robotic device that enables users to easily lift heavy objects.

More interesting is how the robots at the Olympics showcased the convergence of multiple themes. Toyota’s field support robot (FSR) uses AI to avoid collision with obstacles, while its CUE5 humanoid robot used AI to score impressively accurate free throws on the basketball court.20 Creating the human-friendly robots that Japanese society needs inevitably requires a tactful mix of AI and cutting-edge hardware, both of which are qualities that were demonstrated by these two robots.

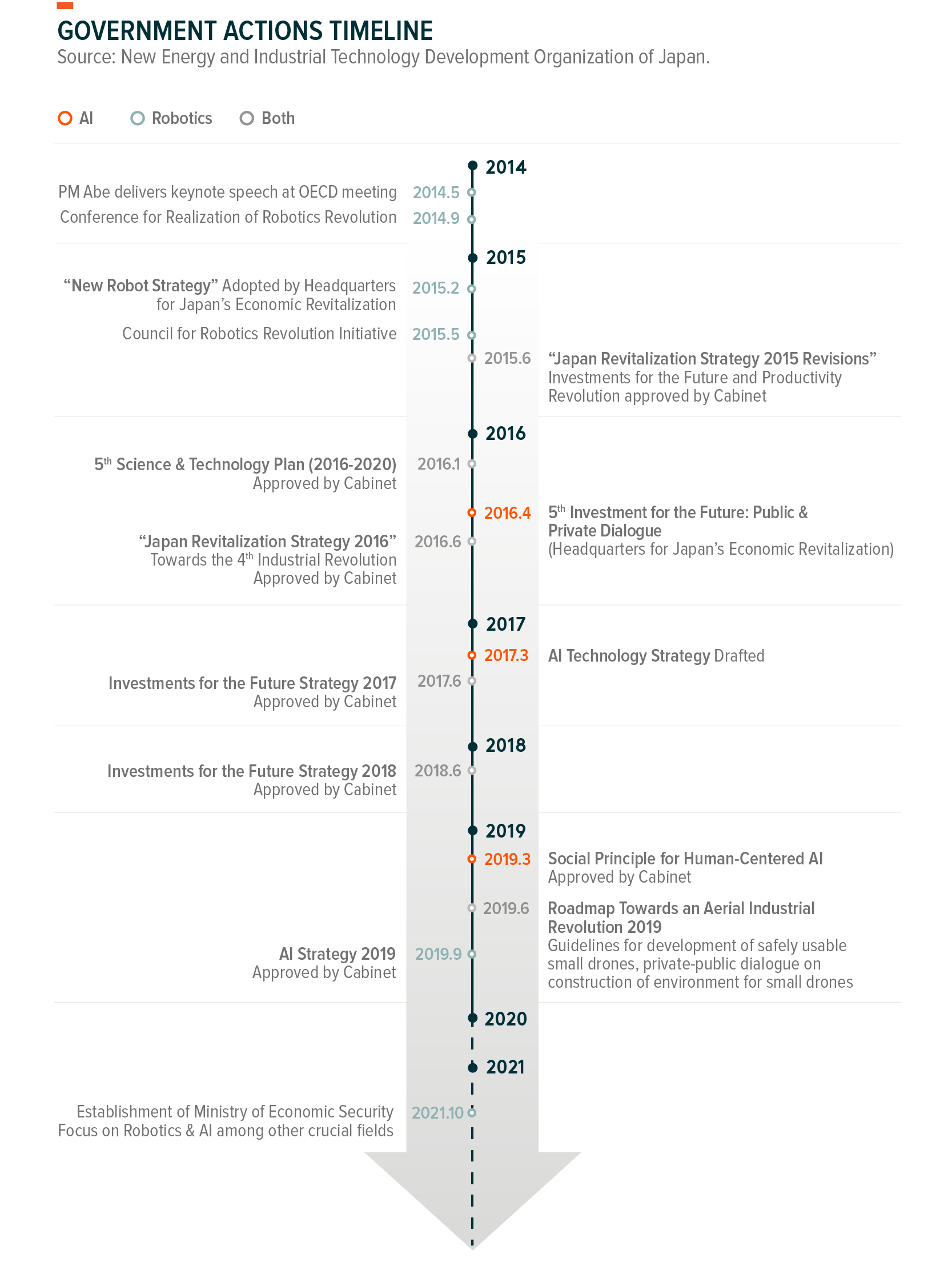

The policies included in this illustration were mostly during Prime Minister Abe Shinzo’s tenure

Recent policy initiatives by the Japanese government reveal that they are aware of the need to support technologies adjacent and complementary to robotics. Nowhere is this clearer than in the Society 5.0 initiative. Proposed in 2016, the initiative states that human society has passed through four levels of development: a hunting society (1.0), an agricultural society (2.0), an industrial society (3.0) and an information society (4.0). The next level of society is Society 5.0, one in which a confluence of disruptive technologies lifts burdens and allow humans to live to their potential. In the vision of the future put forth by Society 5.0, robotics is included alongside trends like the IoT, big data, AI, FinTech and autonomous vehicles.21

Unique structural headwinds drive need for human-friendly bots

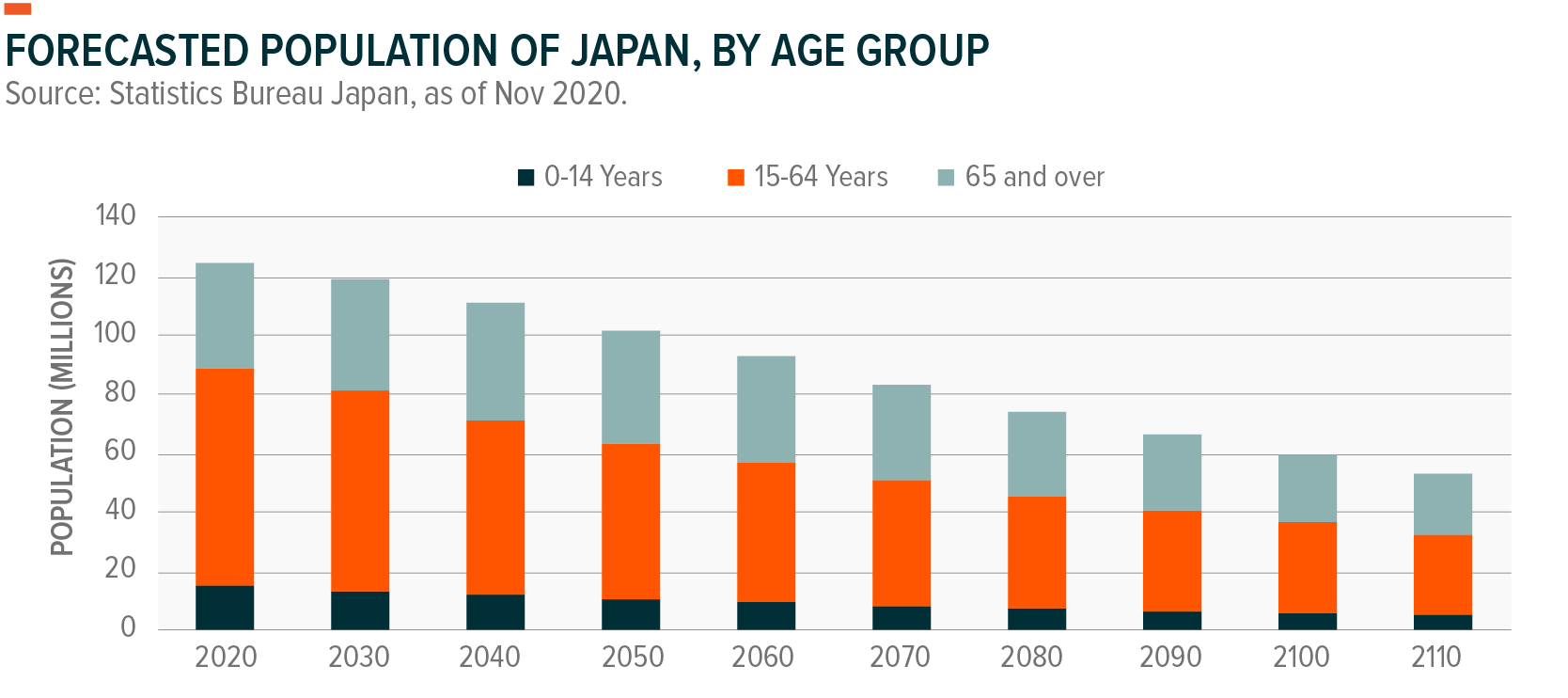

The converging headwinds in Japan of a shrinking labor force, rapid aging and a lack of productivity are making robots increasingly necessary. Japan’s great service robot experiment will set an important precedent for the numerous countries bound to follow Japan’s demographic trends. Making robots palatable to humans will be a critical step towards success in the Society 5.0 experiment.

As the generation that lived through the economic miracle passes away, less young people will be there to replace them. This will not only shrink the labor force, but also create a situation in which fewer adults must take care of more elderly. Robots can mitigate this problem.

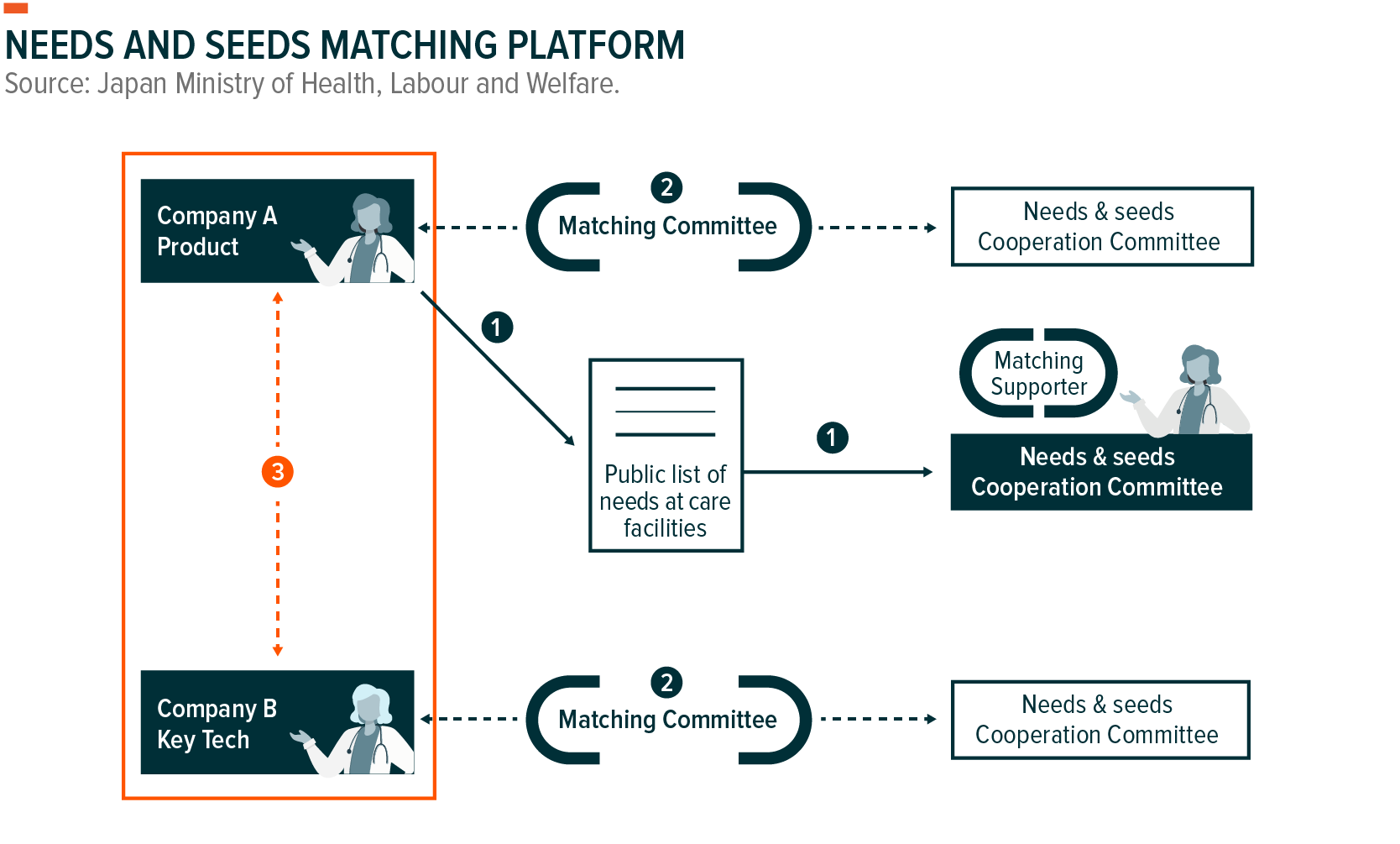

Healthcare and nursing are areas where service robots have great potential. In fact, Japan’s Ministry of Health, Labor and Welfare (MHLW) and METI identified 13 applications and six categories for service robots in nursing. These applications include robots to aid elders in using the restroom, walking around outside and even socializing, and MHLW has policies in place to support the research and adoption of these applications.22 Most recently in July 2021, the MHLW started up the NS Matching Platform, which is a platform to match “needs” with “seeds,” or in other words to connect care facilities in need of robot technology with companies that can provide solutions.23

The MHLW anticipates the number of care workers needed to balloon from 2.33mn to 2.80mn people between 2023 and 2040.24 Robots can help meet these expanding needs by increasing productivity. The NS Matching Platform is just one way the MHLW plans to promote their use among care workers.

Service robots can also brighten up restaurants, hotels, stores, and households. Robots that greet customers during non-peak hours can ease burdens for shops. Although still far from common, more restaurants in Japan are beginning to make use of robotic waiters. The integration of robots into daily life is a key element of Society 5.0.

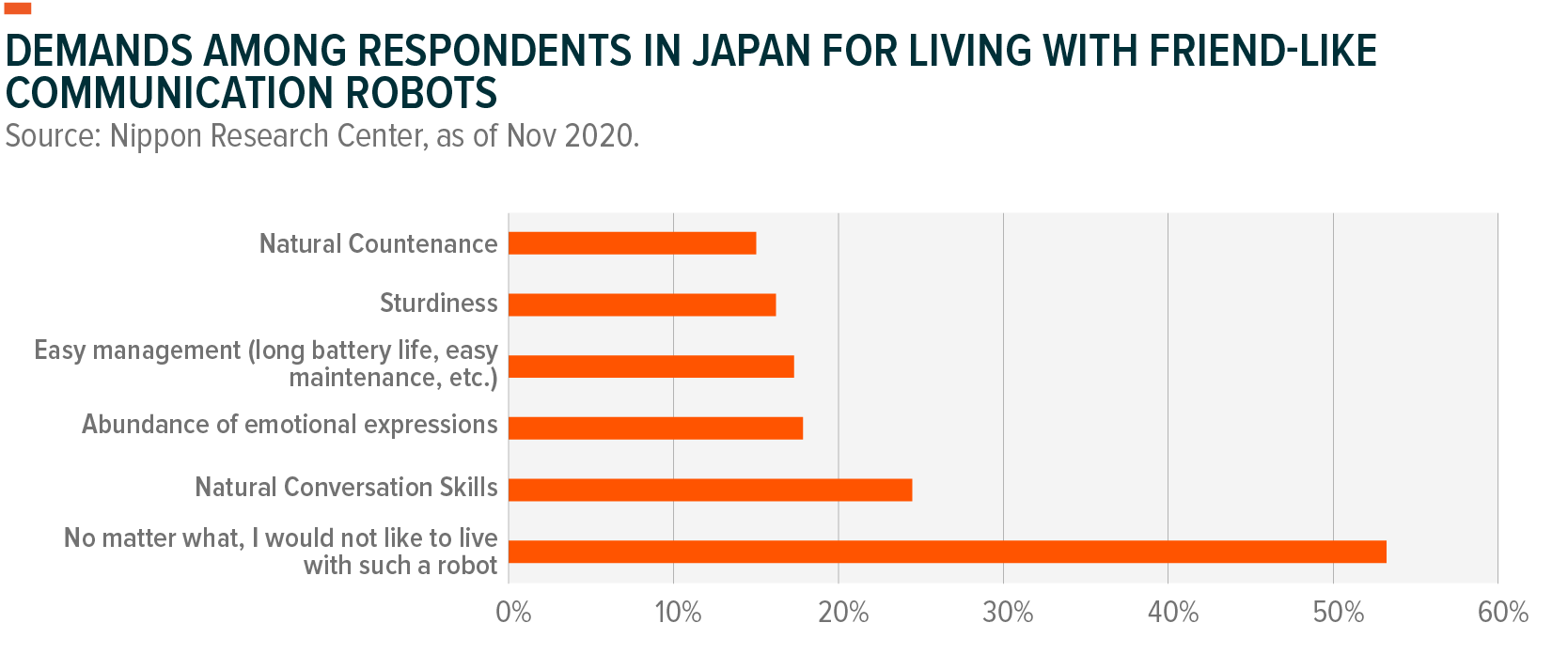

Relatively speaking, the Japanese public does not have a strong aversion to robots, but there is still a long way to go. Palatability and high price tags are obstacles that must be overcome before service robots can truly take off.

COVID-19 crisis sparks innovation

The pandemic accelerated the adoption of numerous disruptive technologies around the world, and it had significant implications for Japan which still lags behind in digitalization despite its high-tech image. COVID exposed difficulties in using hanko seals (personalized stamps used to sign official documents) while working remotely. It also brought attention to excessive reliance on old technology, like the use of fax machines by hospitals to share COVID data. The increased scrutiny towards out-of-date technology is becoming an impetus for further adoption of robotics and automation.

In an era where people must reduce contact with each other, robots have an opportunity to shine. ZMP developed DeliRo, a small four-wheeled robot that drive around the city to carry-out contactless food deliveries. Meanwhile, Hatapro introduced Zukku, a robotic owl that uses AI to greet customers and analyze demand for products based on dialogue with them. Kawasaki also created a set of robotic arms to handle PCR tests at airports.

Conclusion

The tailwinds that helped Japan become a superpower in robotics were a sustained economic miracle, the rise of auto manufacturing and post-war labor shortages. In Japan’s first robotics era, the lion’s share of revenue went to industrial robots. In the year 2021, Japan is faced with drastically different conditions. Unlike the post-war labor shortages, modern Japan’s labor shortages will come from population aging and decline. Meanwhile, new technologies like AI and the IoT are making it easier to integrate human-friendly robots into daily life. These factors are likely to drive the next phase of robotics, as service robots become increasingly integrated into society.

Related ETFs

Please click the fund name above for current fund holdings and important performance information. Holdings are subject to change.