Energy & MLP Insights: Record-High U.S. Oil and Gas Output Requires Midstream Infrastructure

ListenExtended OPEC+ production cuts through year-end and increased demand with economic activity in China picking up are suggesting tighter oil markets for the rest of 2023 and likely into 2024. For U.S. midstream MLPs, we expect an oil market deficit coupled with record U.S. oil and gas production to be a recipe for success, given greater demand for midstream transport systems, warehouses, and factories. As discussed in our previous Energy & MLP Insights, the price environment is likely to remain volatile, but midstream’s defensive contracts and fees structure make it uniquely positioned to benefit compared to other segments of the energy market. With diversification potential and inflation pass-through capabilities core features of the sector, midstream equities can bring unique energy exposure to investor portfolios.

Key Takeaways

- Saudi Arabia and Russia remain aligned in their protracted curtailment of oil production, setting the stage for a likely oil market deficit in Q4.1

- U.S. oil and gas production at an all-time high suggests increased demand for midstream infrastructure.

- Demand for midstream infrastructure is likely to keep the merger and acquisition market active, with the latest example being Energy Transfer LP’s purchase of Crestwood Equity Partners.

Supply Concerns Suggest an Oil Market Deficit Is Likely

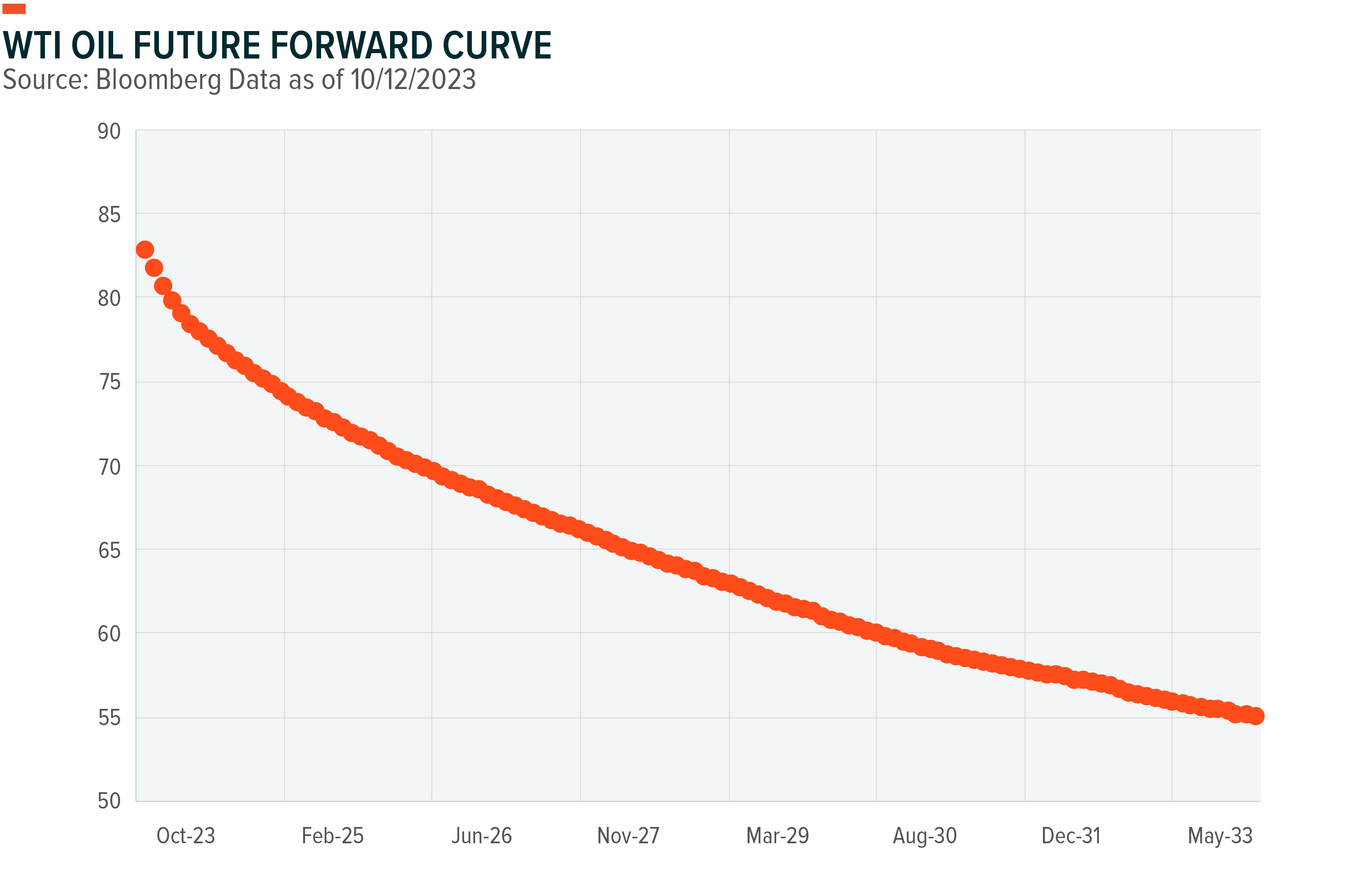

Amidst a confluence of variables including supply reductions and geopolitical tensions, oil futures have lately approached record levels on a consistent upward trajectory throughout the year.2 While the elevated spot prices have the potential to amplify concerns regarding global inflation, the oil futures curve firmly indicates a tight market, by showing a pronounced backwardation.3

Originally slated to end in September, Saudi Arabia announced that it will prolong its voluntary crude oil output cut of 1 million barrels per day (b/d) till the end of the year.4 In August, Russia announced that it would decrease exports by 300,000 bpd through the end of the year.5 These moves pushed oil prices to near record highs and kept global oil supply below demand.

Although the most recent conflict in Israel & Gaza have not had much of an impact on the physical oil markets, it increases the possibility of disruptions in oil supply, which in turn could lead to increased volatility in oil prices.6

On the demand side, unanticipated shifts in global GDP growth in the upcoming months may have an impact on energy consumption because the forecast for the world economy is still uncertain. However, China’s recovery and U.S. weather patterns are in the spotlight. Average global oil consumption is expected to reach a new high in 2023, helped by increased demand from China, the world’s biggest oil importer.7 From July to August, China’s crude imports jumped 21% to 52.8 million tonnes.8 Fresh stimulus measures from Beijing and stronger production from Chinese refiners due to solid export margins contribute to the positive outlook for demand.9,10,11 Finally, amid summer heat in the past few months, strong U.S. air conditioning demand increased natural gas-fired power generation and decreased coal-fired generation.12

Record U.S. Energy Production Puts Midstream Equities in Demand

Saudi Arabia’s production cuts and Russia’s exports cuts may increase price volatility, but U.S. oil and natural gas output can fill global energy market supply gaps with the help of U.S. midstream companies. We think this current production setup represents an opportunity for US midstream companies, given that US producers can step in to fill the void.

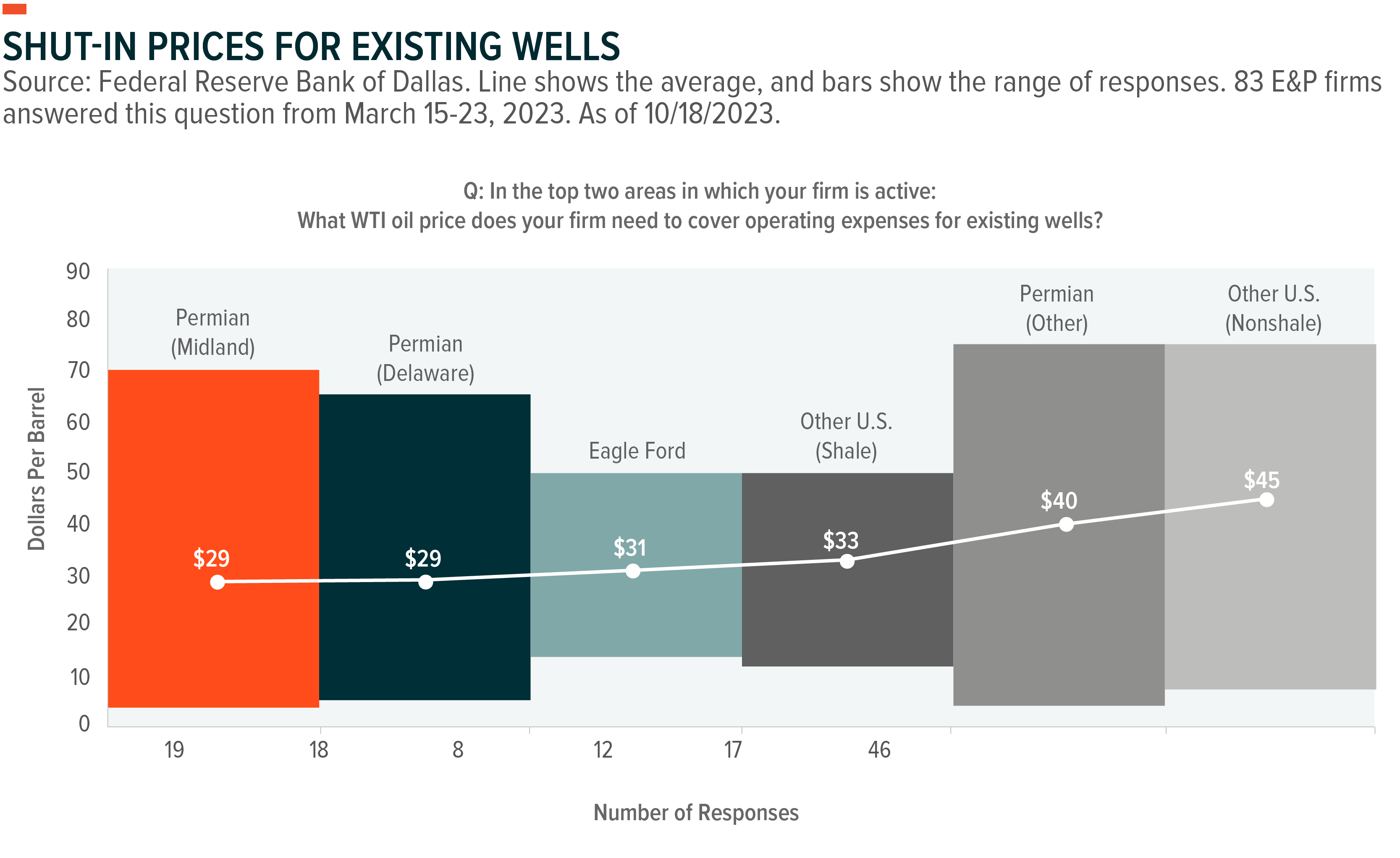

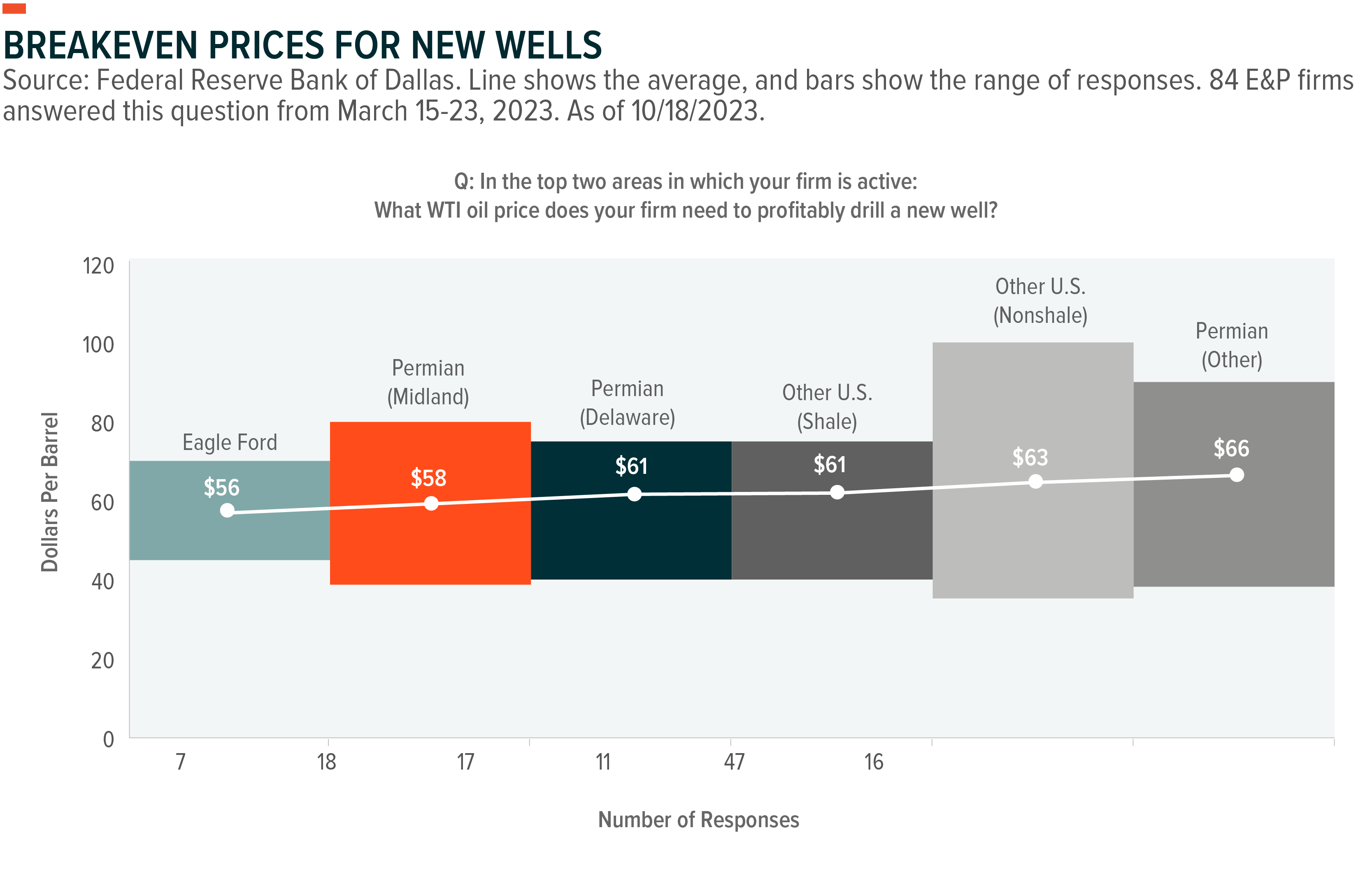

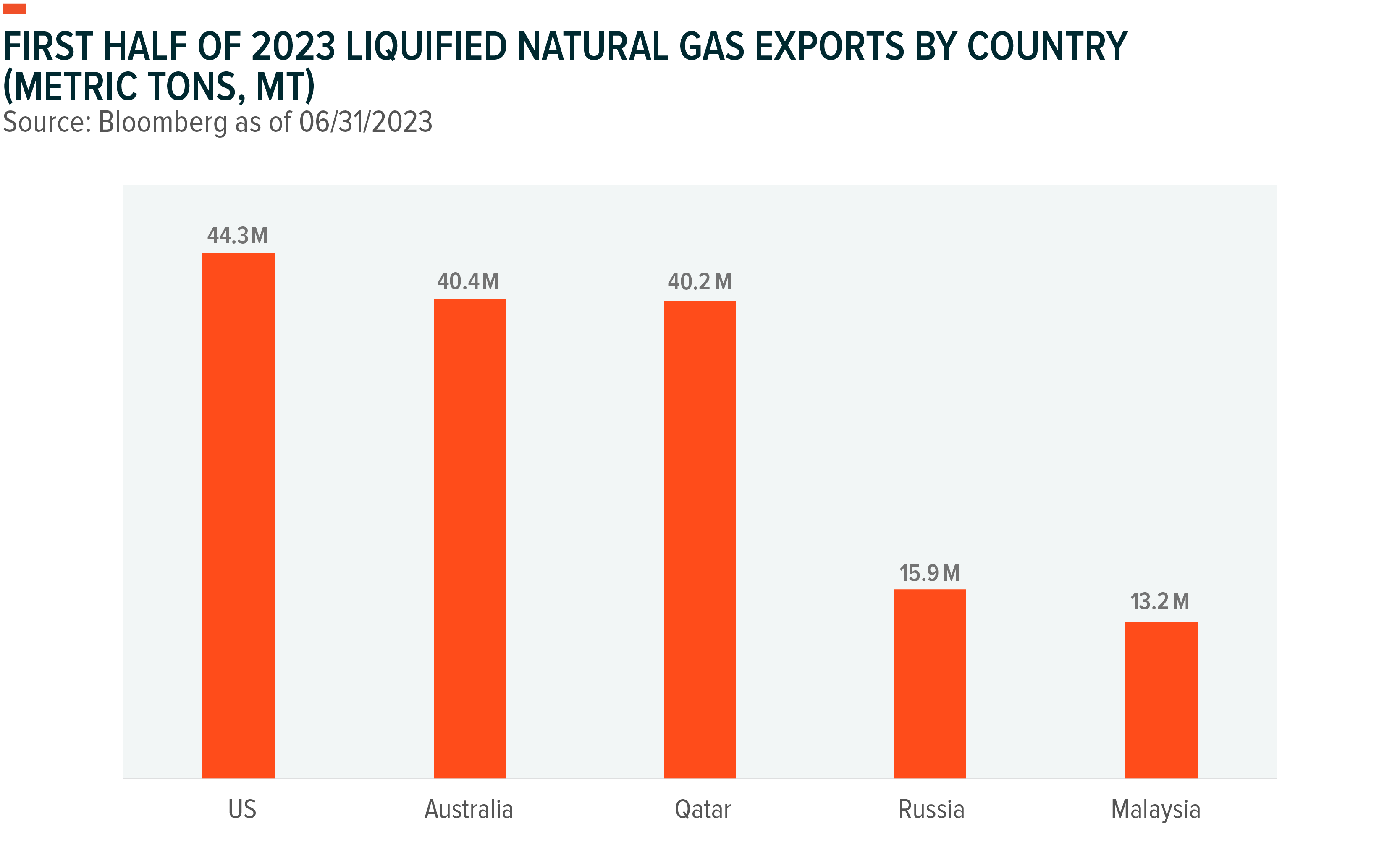

With the WTI price being above the level at which most U.S. oil drilling sites break even, we expect oil rigs, mostly in the Permian Basin, to increase production.13 Also, global export data for first half of 2023 shows that the United States is about to surpass Australia and Qatar as the world’s leading liquefied natural gas supplier.14 Abundant shale resources and foreign buyers’ enthusiasm for U.S. liquefied natural gas (LNG) after moving away from Russian gas due to the war in Ukraine are behind the U.S.’ rise. According to EIA predictions, U.S. natural gas exports might set a record in 2023 and continue to rise in 2024.15

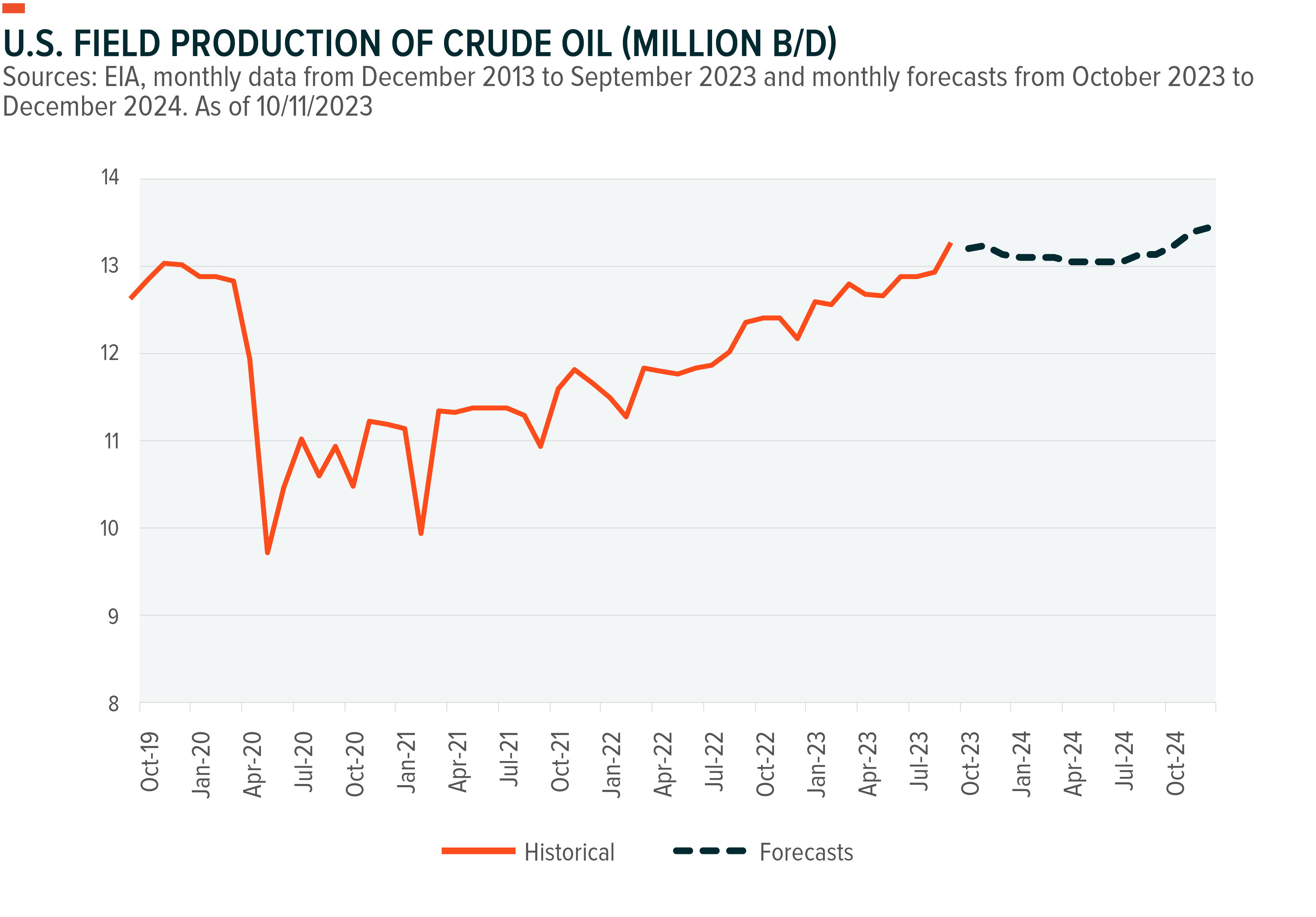

Against this backdrop, the EIA expects non-OPEC global liquid fuels output increase by 2.2 million b/d in 2023 and 1 million in 2024, led by the United States, Brazil, Canada, and Guyana.16 Moreover, they see U.S. oil production averaging 12.92 million barrels a day (Mb/d) in 2023 and 13.12 Mb/d in 2024, or 8% and 10% higher than average production of 11.91 Mb/d in 2022.17

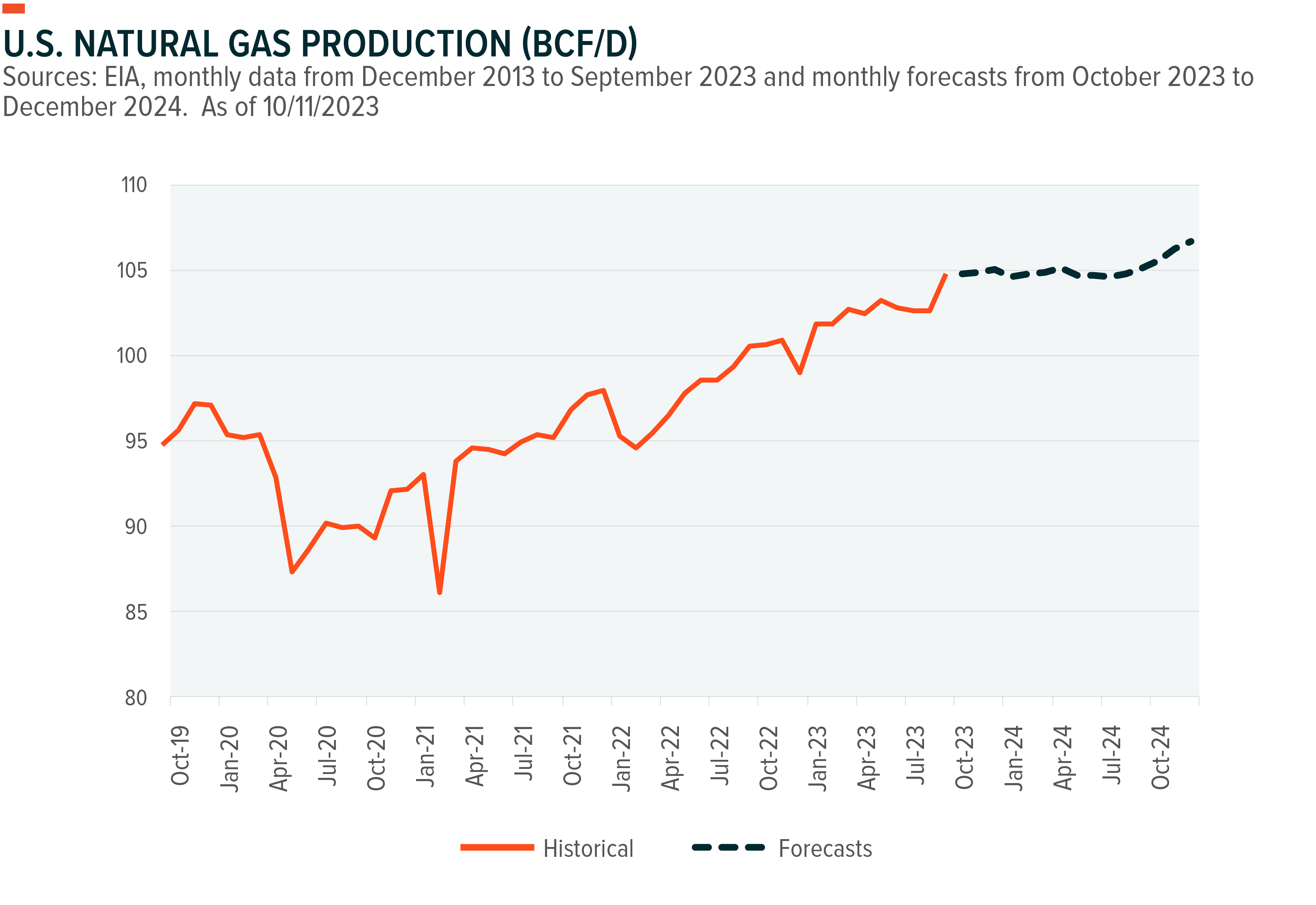

In September, oil output in the United States surpassed the previous record level of barrels per day (bpd) observed prior to the onset of the pandemic and is projected to continue to increase in 2024. The EIA also forecasts U.S. natural gas production to average 103.7 billion cubic feet per day (Bcf/d) in 2023 and 105.1 Bcf/d in 2024, or 6% and 7% higher than average production of 98.07 Bcf/d in 2022, setting the stage for record levels of energy production.18

Mergers & Acquisition (M&A) Activity Helps Midstream Companies to Continue their Strong Performance

Mergers & Acquisition (M&A) Activity Helps Midstream Companies to Continue their Strong Performance

Midstream companies, as measured by the Solactive MLP Infrastructure Index, have performed well year-to-date, increasing by around 22% and outperforming the broader energy sector, measured by the Standard and Poor’s 500 Energy Index, which shows approximately a 7% increase year-to-date as of October 16th, 2023.

The main reasons behind this positive performance are the record US energy production, as previously discussed, and the M&A consolidation in the midstream industry. Indeed, it has been a robust multi-year run of M&A activity in the sector. As we discussed in our last Energy & MLP Insights, M&A can help midstream companies expand their operations quickly, increase their profits, and cut their operating expenses, and in this environment, we expect the deal activity trend to continue.

The latest example is Energy Transfer LP’s acquisition of Crestwood Equity Partners LP in an all-equity deal valued at approximately $7.1 billion, including assumed debt of $3.3 billion.19 Expected to close before year-end, the deal expands Energy Transfer’s footprint in the Williston and Delaware basins and provides an entry point for the Powder River basin.20 The deal also brings commercial synergies to Energy Transfer’s natural gas liquids and refined products business and its crude oil business along with strategically located storage and terminal assets. Energy Transfer expects to achieve at least $40 million of annual run-rate cost synergies before additional benefits of financial and commercial opportunities.21 Crestwood unitholders are projected to benefit from the tax-efficient transaction and have the chance to participate in Energy Transfer’s targeted annual dividend per unit growth rate of 3–5%.22

Earlier this year, Energy Transfer rival Oneok Inc paid $18.8 billion for Magellan Midstream Partners to get access to crude oil transportation and storage markets, a transaction that recently closed. Also, Energy Transfer co-founder and main owner Kelcy Warren bought Lotus Midstream for $1.45 billion.23,24 Moreover, the breadth of this phenomenon extends beyond the realm of midstream mergers and acquisitions: the Exxon transaction that took place was of significant magnitude. At the beginning of October, Exxon Mobil sealed a deal to purchase Pioneer Natural Resources (PXD) for $59.5 billion in an all-stock deal, representing the greatest takeover in over twenty years among oil giants. This latter deal, too, shows renewed momentum in consolidating small-midsize enterprises and large diversified energy producers.25

Conclusion: Oil Supply Crunch Highlights Midstream Energy’s Investment Profile

As long as OPEC+ extends production cuts, more U.S. energy production moves into the spotlight. Rising U.S. oil and gas production combined with a likely oil supply shortfall means midstream’s role as facilitator of the oil and gas market has added significance. Deal activity within the sector can remain high as well with new projects difficult to get off the ground. Even if prices stay volatile, the midstream sector’s fee-based business models and contractual escalators mean they are not as correlated to energy prices as other energy sectors. From a valuation point of view, these companies can also offer strong distribution yields, potentially higher than those of 10-Year Treasuries and REITs, and low valuations, trading at an 8% discount relative to their 5-year average, a greater discount than REITs.26,27 These considerations are two more attractive ingredients in their investment profile.

Related ETFs

MLPX – Global X MLP & Energy Infrastructure ETF

Click the fund name above to view current holdings. Holdings are subject to change. Current and future holdings are subject to risk.